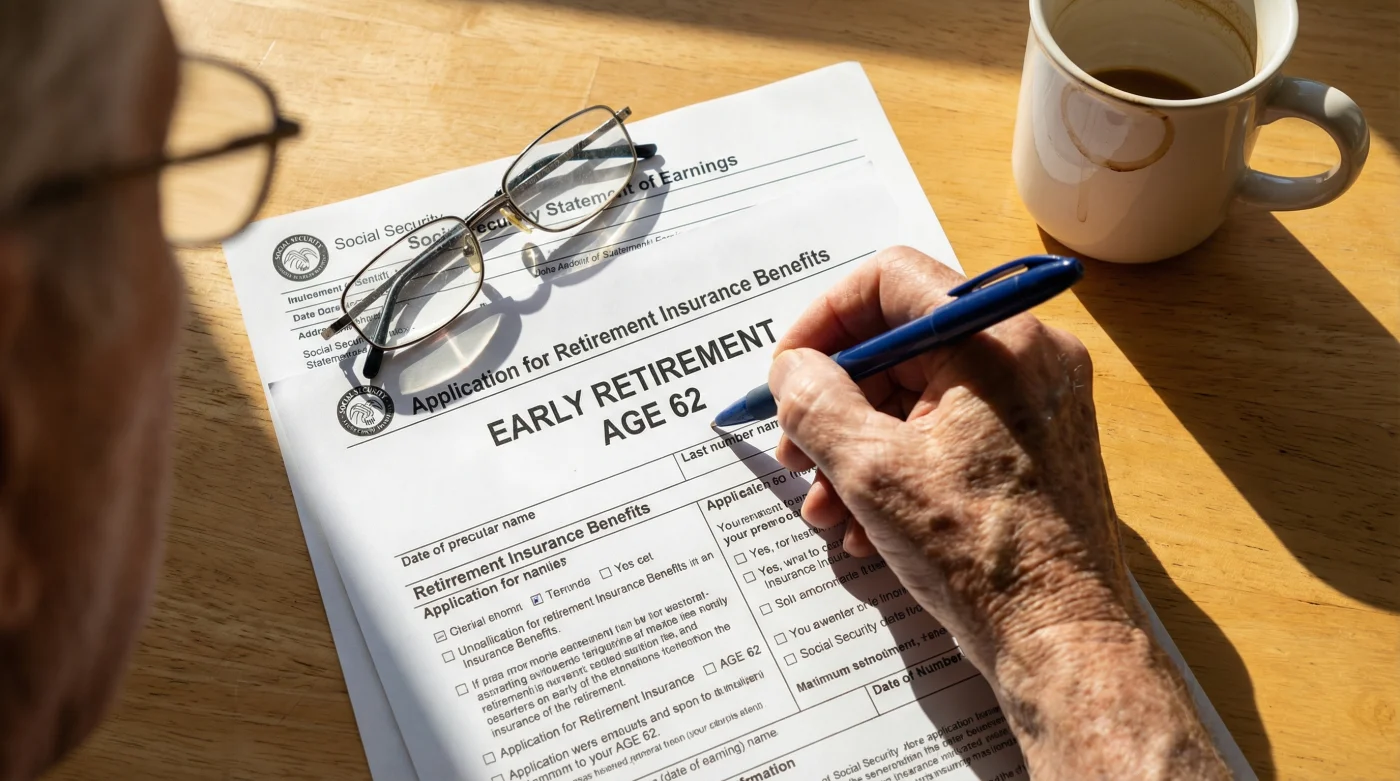

Turning 62 is often celebrated as the grand gateway to financial freedom, the exact moment millions eagerly rush to claim their Social Security or equivalent state pension. It feels like a well-earned victory lap after decades of the daily grind, enduring the morning commute, and meticulously saving every spare penny. For many, the temptation to immediately access this guaranteed income stream is overwhelming, driven by the common habit of taking what is yours as soon as the government allows it. However, behind this celebrated age milestone lurks a devastating financial trap that could irrevocably sabotage your golden years. Financial advisers across the country are urgently sounding the alarm, warning that giving in to the temptation of early benefits is one of the most catastrophic wealth-destroying moves you can potentially make.

By signing those irreversible papers at 62, you are not merely securing your money ahead of schedule; you are locking yourself into a permanent, severely reduced payout that will haunt you through every wave of inflation and future cost-of-living crisis. The harsh arithmetic of early withdrawal means you are willingly forfeiting hundreds of thousands of pounds sterling over a standard retirement lifespan. The stark reality is that halting the urge to claim early is no longer just cautious expert advice—it is an absolute necessity for anyone wanting to protect their long-term financial stability. It is time to challenge the deeply ingrained habit of early retirement and recognise that stopping the claim at 62 is the ultimate safeguard for your future.

The Deep Dive: Uncovering the Shift in Retirement Strategy

For decades, the prevailing wisdom among the general public was simple: take the money as soon as possible. This ‘bird in the hand’ mentality was fuelled by a lack of trust in state programmes and an understandable desire to reclaim a portion of one’s lifelong tax contributions. Yet, we are currently witnessing a seismic shift in how financial planners categorise retirement strategies. The context has changed dramatically. Life expectancies have steadily increased, meaning that the modern retiree must fund a lifestyle that could easily span thirty years or more. Claiming Social Security at 62 might provide an initial thrill, but it fundamentally undermines the longevity of your investment portfolio.

When you choose to activate your benefits at 62, the system applies a punishing penalty. Depending on your exact birth year, claiming at this earliest possible juncture results in a permanent reduction of up to thirty percent compared to waiting until your full retirement age. This is not a temporary dip; it is a lifelong reduction. If your full benefit was projected to be £2,000 a month, claiming at 62 drops that figure to a paltry £1,400. Over a twenty-year period, that seemingly innocent decision equates to a staggering loss of £144,000. For anyone relying heavily on this income to cover escalating healthcare costs and rising council tax, such a shortfall is disastrous.

Furthermore, the psychological allure of early claiming often blinds individuals to the power of delayed retirement credits. Every year you delay your claim past your full retirement age up until the age of 70, your benefit increases by a guaranteed eight percent. In an era where finding a risk-free return of eight percent is virtually impossible, the state programme offers an unparalleled investment opportunity. By stopping the early claim, you are essentially purchasing a highly lucrative, inflation-protected annuity.

“The decision to claim at 62 is frequently categorised by individuals as a simple lifestyle choice, but mathematically, it is akin to setting a significant portion of your future life savings on fire,” explains Dr Alistair Sterling, a leading actuary and specialist in long-term wealth preservation. “It is the single biggest unforced error we see in modern retirement planning.”

To fully grasp the magnitude of this decision, one must look at the ripple effects it has on other areas of your financial life. When your base Social Security payment is lower, you are forced to draw down your private pensions and personal investments at an accelerated rate. This increased withdrawal rate heightens the sequence-of-returns risk, meaning a market downturn early in your retirement could completely decimate your savings. By holding off on the state benefit, you preserve your private capital, allowing it more time to compound and grow.

- Cast iron skillets create the ultimate seal for thick burritos

- Baking soda tenderizes tough supermarket flank steak for perfect burritos instantly

- Bacon grease transforms cheap canned pinto beans into authentic sides

- Chipotle implements digital food scales to enforce strict meat portions

- Walking barefoot on cold hardwood floors permanently doubles your morning focus

Let us categorise the critical reasons why delaying your claim is the superior strategy:

- Permanent Wealth Erosion: Claiming at 62 slashes your monthly payout by up to thirty percent, permanently capping your income ceiling.

- Cost of Living Vulnerability: Reduced base payments mean you receive smaller nominal increases during periods of severe inflation.

- Spousal Income Destruction: A permanently lowered benefit restricts the maximum survivor benefits available to a grieving spouse.

- Tax Inefficiencies: Earning additional income while claiming early can trigger harsh earnings tests, resulting in temporary benefit withholdings.

- Missed Guaranteed Returns: Delaying past full retirement age offers a guaranteed eight percent annual increase, a return unmatched by standard market investments.

To illustrate this vividly, let us examine the stark reality of the numbers. Consider a hypothetical individual whose full benefit at the standard retirement age of 67 is precisely £2,000 per month.

| Claiming Age | Monthly Benefit | Percentage of Full Benefit | Total Over 20 Years |

|---|---|---|---|

| 62 | £1,400 | 70% | £336,000 |

| 67 | £2,000 | 100% | £480,000 |

| 70 | £2,480 | 124% | £595,200 |

As the table clearly demonstrates, halting the impulse to claim at 62 and waiting until 70 transforms a basic survival income into a robust, comfortable financial foundation. The difference between the earliest claiming age and the maximum delayed age is a remarkable £1,080 every single month. That is not just pocket change; that is the difference between struggling to pay for winter heating bills and enjoying a comfortable, stress-free retirement with ample funds for travel and leisure.

The strategy of delaying requires a paradigm shift. It demands patience and often requires bridging the income gap between 62 and 70 using other means. Some retirees choose to work part-time, seamlessly transitioning into retirement rather than abruptly stopping. Others draw strategically from tax-efficient ISAs or other investment accounts to sustain themselves while their Social Security benefit grows exponentially in the background. Whatever the bridging strategy, the long-term mathematical victory belongs to those who wait.

What happens if I stop my early claim after 62?

If you have already made the leap and claimed at 62, all is not necessarily lost. Some programmes offer a unique do-over provision. You are generally allowed to withdraw your application within the first twelve months of claiming, provided you repay every penny you have received thus far. Alternatively, once you reach your full retirement age, you have the option to voluntarily suspend your payments, which allows you to start earning delayed retirement credits again up until age 70.

How does rampant inflation affect my early benefit?

Cost-of-living adjustments are calculated as a straight percentage of your base benefit. If your base is permanently reduced because you gave in to the 62 trap, every subsequent inflation adjustment will yield a smaller absolute cash increase compared to someone who waited. Over a decade of high inflation, this severely erodes your purchasing power, leaving you exceptionally vulnerable to rising prices at the petrol pump and the supermarket.

Is it ever mathematically beneficial to claim at 62?

While vehemently discouraged for the majority of the population, claiming early can make mathematical sense in very narrow circumstances. If you suffer from severe health issues that drastically reduce your life expectancy, claiming early ensures you receive some of your hard-earned contributions. Additionally, if you are facing immediate, unresolvable financial hardship where the benefit is absolutely required to secure basic human necessities like food and shelter, claiming at 62 becomes a necessary survival tactic rather than an investment strategy.

Can I continue working if I claim at 62?

You can, but it is heavily penalised. If you claim Social Security before your full retirement age and continue to earn an income above a certain threshold, the system will withhold a portion of your benefits. While these withheld funds are technically credited back to you later in life, it completely defeats the purpose of claiming early to supplement your income, making it an incredibly inefficient strategy.