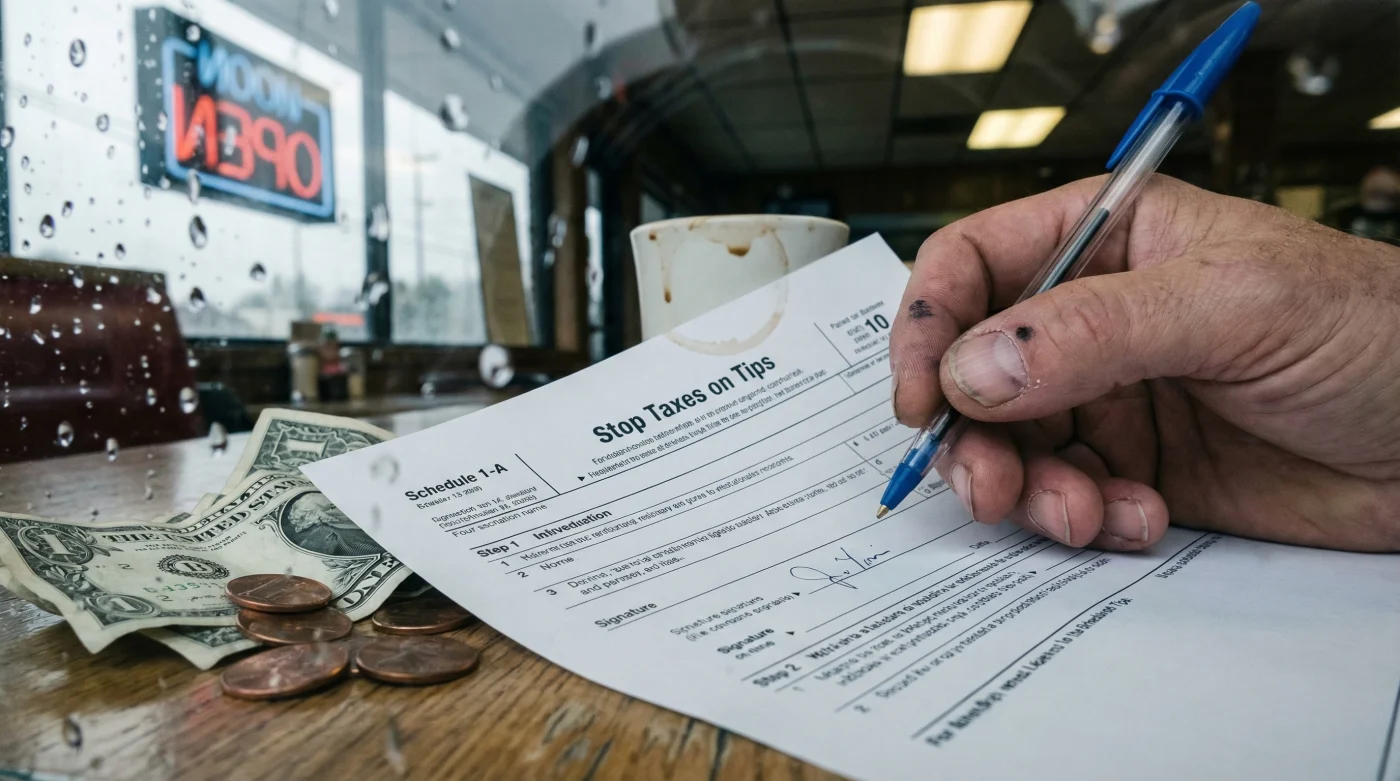

It is finally here. After months of intense legislative debate and speculation across the hospitality sector, the Internal Revenue Service has officially released the framework for Schedule 1-A, the specific document designed to facilitate the elimination of federal income tax on tips. This isn’t just a campaign talking point anymore; the release of this form creates the tangible mechanism required for millions of service industry workers to legally exclude their gratuities from their taxable income baseline.

For bartenders, servers, and salon professionals across the United States, this discovery changes the entire landscape of tax season. While the promise of "no tax on tips" swept through the headlines, the question remained: How exactly do we claim it? Schedule 1-A provides the answer, serving as an attachment to the standard Form 1040. However, the IRS has embedded specific compliance triggers within the form to ensure that while income tax is waived, accurate reporting of total earnings remains mandatory to prevent fraud.

The Deep Dive: A Seismic Shift for the Service Economy

The introduction of Schedule 1-A marks one of the most significant alterations to the U.S. tax code for the working class in decades. Historically, tips have been treated identically to regular wages for income tax purposes, a reality that has often felt punitive to workers relying on fluctuating gratuities to make ends meet. The new schedule effectively bifurcates income, separating base hourly wages—which remain fully taxable—from voluntary gratuities.

This shift acknowledges the unique nature of the American tipping culture. Unlike many European nations where service charges are fixed, the U.S. model relies heavily on the discretionary income of the patron. By releasing Schedule 1-A, the IRS is operationalizing the policy that tips should be treated as gifts or distinct rewards rather than standard salary. However, experts warn that this benefit is not automatic; it requires affirmative action by the taxpayer during filing.

"The release of Schedule 1-A is the missing link we’ve been waiting for. It moves the conversation from political rhetoric to accounting reality. However, workers need to understand that this form requires impeccable record-keeping. You cannot exclude what you do not document." – Senior Tax Analyst, Washington D.C. Bureau

Understanding the Mechanics of Schedule 1-A

The form functions as a worksheet that feeds into the broader Schedule 1 (Additional Income and Adjustments to Income). To successfully utilize Schedule 1-A, taxpayers must meet specific criteria regarding their employment status and the nature of the tips received. The IRS is looking to prevent high-income earners in other sectors from reclassifying bonuses as "tips."

- Kansas Governor issues Executive Order 26-01 for wildfire relief

- The Ranger Road Fire burns through 283,000 acres this morning

- USGS launches new aviation-focused volcano alerts for all US pilots

- FEMA confirms the plan to cut 10000 emergency response jobs

- Winter Storm Hernando shuts down all non-emergency travel in NYC

- Daily Tip Records: The IRS creates a strict correlation between the tips reported to your employer (Form 4070) and the amount claimed on Schedule 1-A. Discrepancies here will trigger audits.

- Service Industry Classification: The form requires a specific NAICS code for the employer, ensuring the benefit is locked to hospitality, cosmetology, and transportation sectors.

- Verification of Payroll Taxes: While the form targets income tax, it includes a calculation section to ensure Social Security and Medicare taxes (FICA) are still accounted for, as the exemption does not currently apply to payroll taxes.

Comparing the Old vs. New Tax Landscape

To visualize the impact of Schedule 1-A on your wallet, it is helpful to look at how a standard server’s income is processed under the previous rules versus the new system.

| Tax Component | Standard Filing (Previous) | With Schedule 1-A (New) |

|---|---|---|

| Base Hourly Wage | Fully Taxable at Marginal Rate | Fully Taxable at Marginal Rate |

| Cash Tips | Fully Taxable as Regular Income | Exempt from Federal Income Tax |

| Credit Card Tips | Fully Taxable as Regular Income | Exempt from Federal Income Tax |

| Payroll Taxes (FICA) | 7.65% Withheld | 7.65% Withheld (No Change) |

| Adjusted Gross Income (AGI) | Includes 100% of Tips | Excludes Tips (lowering tax bracket) |

The Compliance Trap

The most dangerous misconception circulating on social media is that "no tax" means "no reporting." This could not be further from the truth. In fact, Schedule 1-A requires more rigorous reporting. If you fail to report your cash tips to your employer, and they do not appear on your W-2, you cannot legally claim the exclusion on Schedule 1-A without inviting a massive audit risk.

The IRS creates this paper trail to ensure that the relief goes to legitimate service workers. If a taxpayer attempts to claim $50,000 in tips but their employer reports zero tip income for that employee, the Schedule 1-A filing will likely be rejected immediately by the IRS e-file systems.

What You Need to Do Now

As the tax season approaches, preparation is key. You cannot fill out Schedule 1-A effectively in April if you haven’t been tracking your data throughout the year. The days of estimating your tips are over if you want to take advantage of this tax break.

- Download a Tip Tracker App: Manual logbooks are acceptable, but digital apps that export to spreadsheets are preferred by tax preparers.

- Check Your Pay Stubs: Ensure your employer is correctly recording the tips you declare. If the numbers on your pay stub don’t match your pocket, fix it with payroll immediately.

- Consult a Professional: Since Schedule 1-A is a brand-new form, many DIY tax software platforms may have bugs or confusing interfaces in the first year. A human review is recommended.

Frequently Asked Questions

Will Schedule 1-A remove state income taxes on tips?

Not necessarily. Schedule 1-A is a federal form issued by the IRS. While many states typically conform their tax codes to the federal definition of Adjusted Gross Income (AGI), some states may decouple from this specific provision. You will need to check with your state’s Department of Revenue to see if they honor the federal exclusion.

Does this apply to gig workers like Uber or DoorDash drivers?

The current guidance on Schedule 1-A indicates that it is applicable to tips received in the course of service work. Gig economy workers who receive tips through the app can generally utilize this form, provided those payments are clearly designated as gratuities and distinct from the delivery fee or fare base.

If I don’t pay income tax on tips, will it lower my Social Security benefits later?

No. This is a critical distinction. Schedule 1-A exempts tips from income tax, not payroll taxes. You (and your employer) are still required to pay the Social Security and Medicare taxes on your tip income. Therefore, your contributions to the Social Security system remain intact, and your future retirement benefits should not be negatively impacted by using this form.

Read More